If you've been wondering what's happening in the Ottawa real estate market, you're definitely not alone.

Over the past few weeks, I've been getting questions like:

"Steve, are homes still selling?"

"Have prices dropped?"

"Is it a buyer's market now?"

"Should I wait until the fall?"

Let's sit down over a coffee and talk about what the numbers are really telling us, without all the confusing headlines.

So... What's Happening in the Ottawa Housing Market?

The good news is that Ottawa's housing market remains balanced.

Think of it this way...

Buyers have more homes to choose from than they've had over the past few years, but well-priced homes are still attracting serious interest. We're no longer seeing the frantic bidding wars that became common a few years ago, but we're also not seeing prices collapse.

Instead, we're seeing a healthier market where buyers can take a little more time to make informed decisions, while sellers who price their homes correctly are still achieving excellent results.

That's good news for everyone.

Home Sales Slowed Slightly... But That's Normal

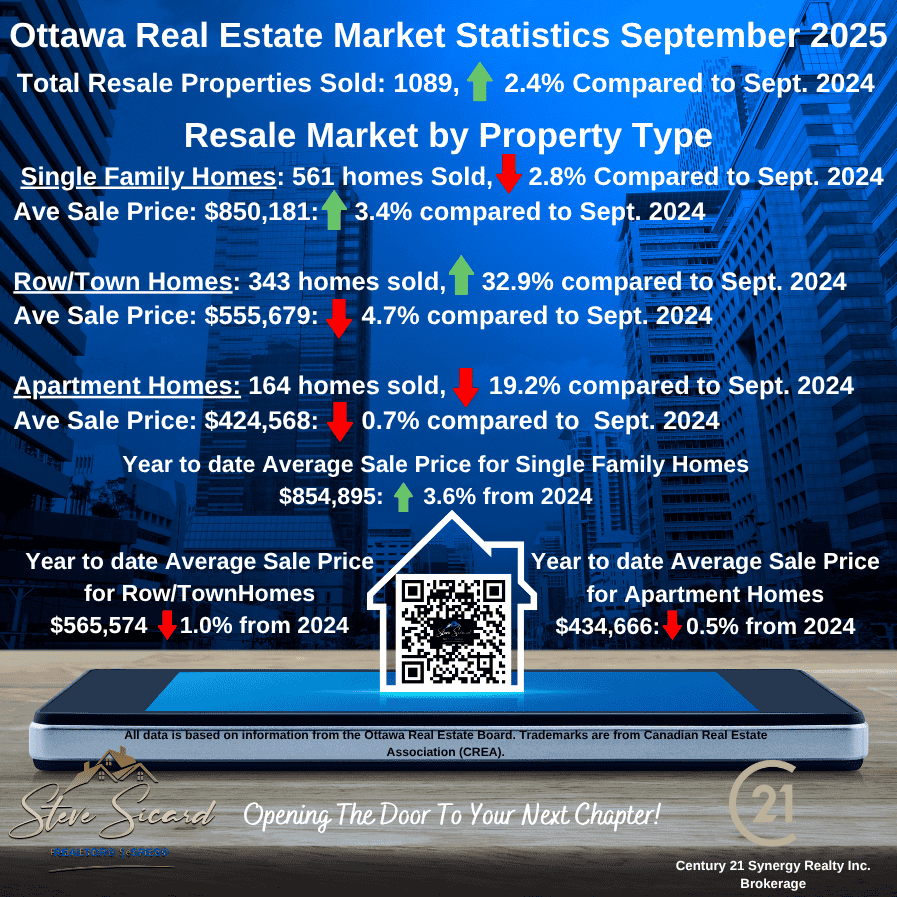

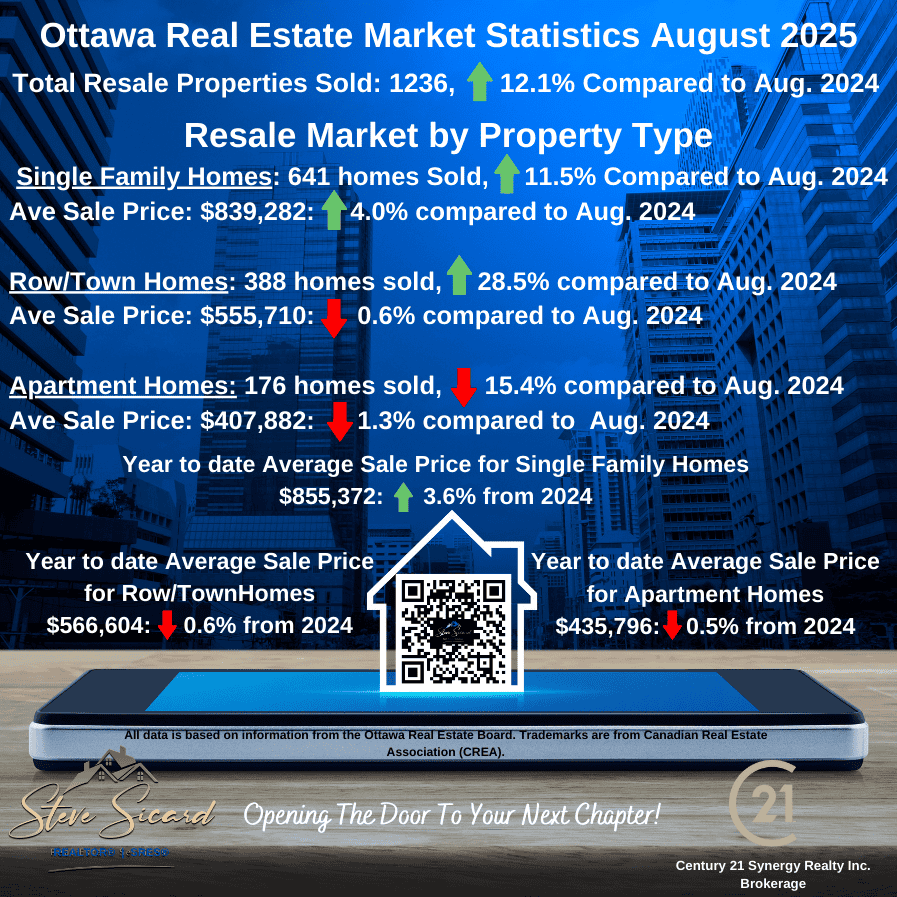

In June 2026, 1,518 homes sold through Ottawa's MLS® System.

That's about 5% fewer sales than June of last year, and slightly below May's total.

Before anyone panics...

This is actually quite typical.

Every year, once school begins to wrap up, vacations start, and families focus on summer activities, the real estate market naturally eases off from the busy spring pace.

So while sales were a little lower, the seasonal pattern isn't surprising.

More Homes on the Market Means More Choices

One of the biggest changes this year is inventory.

There are simply more homes available than buyers have seen over the past several years.

If you're buying, that's welcome news.

Instead of feeling rushed into making an offer on the first property you like, you can compare neighbourhoods, layouts, prices and features before making one of the biggest financial decisions of your life.

That doesn't mean sellers can't be successful.

It simply means pricing, presentation and marketing have become much more important than they were during the pandemic frenzy.

Not Every Type of Home Is Performing the Same

Here's where the market gets interesting.

When people hear "Ottawa housing market," they often assume every property is behaving the same way.

That's simply not true.

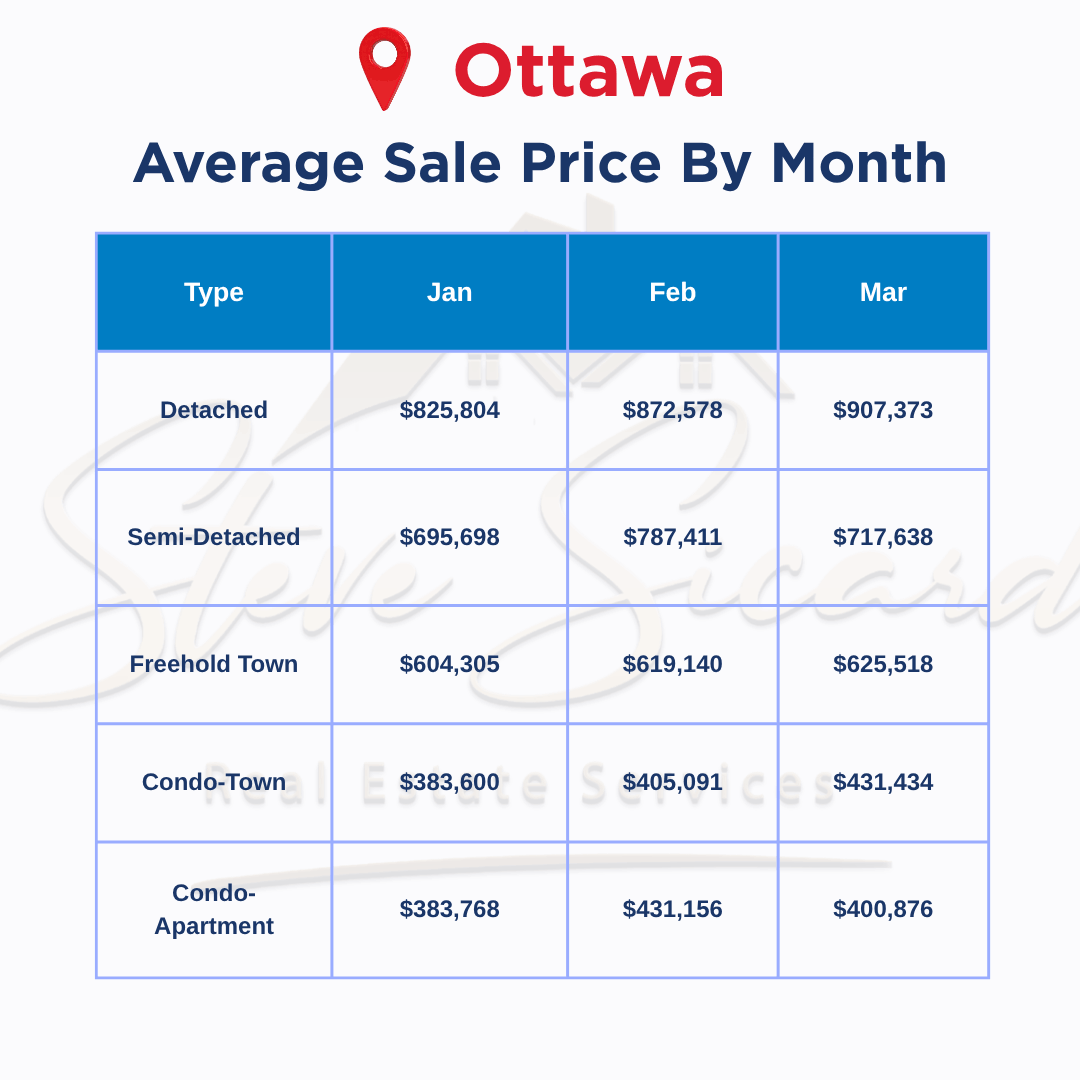

Single-Family Homes Continue to Lead

Detached homes remain the strongest segment of the market.

Demand has stayed relatively steady, inventory remains manageable, and these homes continue attracting the greatest number of buyers.

If you're selling a detached home that's priced appropriately and shows well, you're still in a very good position.

Townhomes Are a Little More Competitive

Townhomes remain popular, but they're seeing a bit more competition as inventory grows.

That means buyers have more options, making pricing even more important for sellers.

Condominiums Continue to Face the Biggest Challenges

Apartment-style condominiums remain the softest part of Ottawa's real estate market.

With more inventory available, buyers have greater negotiating power, meaning condo sellers need to be especially strategic when preparing and pricing their homes.

What About Home Prices?

This is where headlines can become confusing.

The average residential sale price in Ottawa during June was $733,648, which is 1.3% higher than one year ago.

However...

The median sale price was $655,000, which is 1.3% lower than last June.

How can both be true?

Because average prices can be influenced by more expensive homes selling during the month.

Median prices often provide a clearer picture of where the "middle" of the market sits.

The takeaway?

Prices remain relatively stable.

We're not seeing dramatic increases, but we're also not seeing widespread price declines.

Homes Are Still Selling Close to Asking Price

One statistic that often gets overlooked tells us a lot about today's market.

Homes sold for an average of 98.5% of their asking price, virtually unchanged from last year.

That tells us buyers are negotiating—but not dramatically.

Sellers who price realistically are still receiving very strong offers.

Homes Aren't Sitting on the Market Much Longer

Another encouraging sign?

The median days on market increased only slightly—from 19 days to 22 days.

That's hardly a major slowdown.

Instead, it suggests buyers are taking a little more time to make thoughtful decisions rather than rushing into offers.

For many people, that's actually a healthier market.

Why Local Neighbourhood Knowledge Matters More Than Ever

One of the biggest mistakes buyers and sellers make is relying solely on city-wide statistics.

Ottawa isn't one market.

It's dozens of neighbourhood markets.

What's happening in Orléans can be very different from Barrhaven.

Kanata may perform differently than Alta Vista.

Condominiums in downtown Ottawa can behave very differently from detached homes in Cumberland.

That's why local knowledge has become more valuable than ever.

Understanding your specific neighbourhood, property type, price range and current buyer demand often makes a much bigger difference than any city-wide headline.

So... Is Now a Good Time to Buy or Sell?

Honestly?

For many people...

Yes.

If you're buying, you'll likely appreciate having more selection and fewer bidding wars.

If you're selling, properly priced homes continue to attract serious buyers and sell close to asking price.

The key isn't trying to "time the market."

The key is making sure your decision fits your life, your finances and your future plans.

Final Thoughts

The Ottawa real estate market in June 2026 continues to demonstrate stability.

Inventory is higher than we've seen in recent years, giving buyers more choice while encouraging sellers to price strategically.

Detached homes remain the strongest market segment, townhomes continue to perform well with proper pricing, and condominiums are presenting the greatest opportunities for buyers.

If you're thinking about buying, selling, downsizing, rightsizing, or simply wondering what your own neighbourhood is doing, remember that every area of Ottawa tells a different story.

Having accurate, local information can make all the difference.

I'd be happy to sit down over a coffee for a no-obligation conversation about your goals, answer your questions, and help you understand exactly what's happening in your neighbourhood—so you can make confident decisions when the time is right.

Frequently Asked Questions About the Ottawa Housing Market

Is Ottawa currently a buyer's market?

Ottawa remains a balanced real estate market. Buyers have more inventory and choice than in recent years, but well-priced homes continue to sell successfully.

Are Ottawa home prices falling?

Overall prices have remained relatively stable. While the median price dipped slightly compared to last year, average sale prices increased modestly, reflecting differences in the types of homes being sold.

What type of home is selling best in Ottawa?

Single-family detached homes continue to show the strongest demand, followed by townhomes. Apartment-style condominiums remain the softest market segment.

Should I wait to buy or sell?

Every situation is different. Rather than trying to predict the market, it's usually better to make your decision based on your personal goals, finances and lifestyle, while understanding what's happening in your specific neighbourhood.

Ready to Talk About Your Situation?

Every homeowner's circumstances are unique. Whether you're thinking about buying, selling, downsizing, rightsizing, or simply wondering what your home might be worth in today's Ottawa real estate market, I'd be happy to help.

Let's have a relaxed, no-obligation conversation about your goals, answer your questions, and explore the options that make the most sense for you.

👉 Want to discuss your personal situation? Click here to book your complimentary consultation.